Search intent answer

personal injury protection PIP

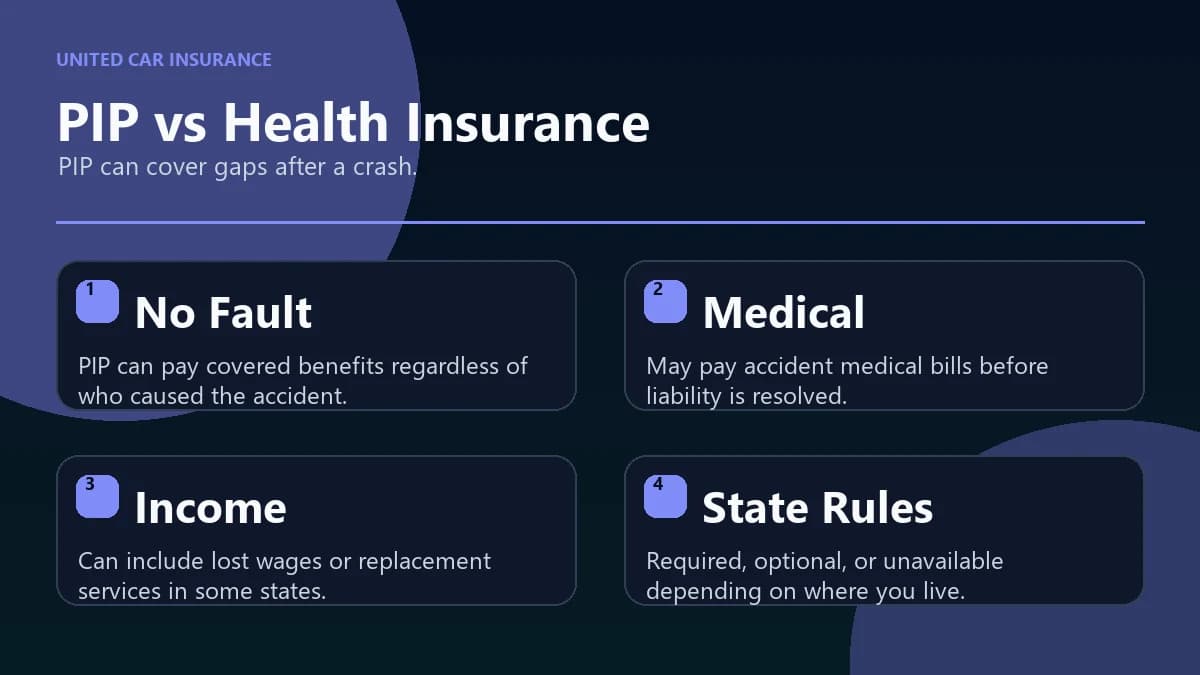

Personal Injury Protection, or PIP, can pay medical expenses and sometimes lost wages or replacement services after a car accident, regardless of who caused the crash. Availability, limits, and requirements vary by state.

Reader goal

Understand whether PIP fills gaps left by health insurance and liability claims.

What this page helps you decide

- Check whether PIP is required, optional, or unavailable in your state.

- Compare medical, wage-loss, funeral, and replacement-service benefits.

- Review deductibles and health insurance coordination rules.

- Know claim deadlines and required medical documentation.

The 30-Second Briefing

- ▸ The "Health Insurance" Myth: Your health plan has a $2,500 deductible and covers zero lost wages. PIP covers both.

- ▸ The "Lost Wage" Safety Net: PIP is the only auto coverage that pays 60-80% of your paycheck while you recover.

- ▸ The 2026 Shake-Up: Florida is moving (potentially) from No-Fault to Tort in July. Michigan now has tiered limits. Know your state's new rules.

- ▸ The "Coordination" Trap: Setting health insurance as "Primary" lowers your premium but can delay care if your HMO denies the accident claim.

Ask 10 drivers what Personal Injury Protection (PIP) covers, and 9 will say, "It pays my medical bills if I get hurt."

They then follow up with, "But I already have Blue Cross/Aetna, so why am I paying for this?"

This misunderstanding costs people thousands of dollars every year. PIP isn't just "medical" insurance. It is Disability Light. It is Childcare Insurance. It is a Cash Advance protecting your family from bankruptcy while the insurance companies fight over who ran the red light.

Part 1: The "Health Insurance Gap"

Why do you need auto medical coverage if you have health insurance? Because your health insurance has holes in it.

PIP vs. Your Health Plan (The Reality)

| Feature | Your Health Plan (HMO/PPO) | PIP (No-Fault) |

|---|---|---|

| Deductible | $1,500 - $5,000 (Average) | $0 - $1,000 (You choose) |

| Lost Wages | $0 (Not covered) | 60-85% of Income (Up to limit) |

| Household Help | $0 (Clean your own house) | Pays for cleaning/childcare |

| Network | Strict (In-Network Doctors only) | Flexible (Any licensed provider) |

| Speed of Payment | Slow (Weeks/Months) | Fast (Usually within 30 days) |

Part 2: The "Lost Wage" Lifeline

This is the most overlooked benefit. If you break your leg in a crash and can't stand at your job for 6 weeks, your health insurance won't pay your rent. Your Liability Coverage pays the other guy, not you.

How It Works

You submit a "Wage Verification" form from your employer. PIP pays you every 2 weeks, just like a paycheck, usually at 60% (FL) or 85% (MI) of your gross income, up to the policy limit (e.g., $10,000).

The "Household Services" Bonus

If you are a stay-at-home parent, you don't have "wages." But PIP (in many states) pays for "Replacement Services"—hiring someone to clean the house, mow the lawn, or care for kids while you recover.

Part 3: The 2026 Landscape (State Shake-Up)

No-Fault laws are messy boundaries. Where you live determines your strategy.

Florida: The Big Shift (July 2026)

Florida legislature has been battling to repeal No-Fault for years. If the new bill passes effective July 1, 2026, mandatory PIP vanishes.

- Old Rule: $10k PIP required.

- New Rule (Proposed): $25k Bodily Injury Mandatory + Mandatory MedPay.

- Strategy: Even if PIP becomes optional, keep it. The wage loss benefit is unmatched.

- Check updates at FLHSMV.gov.

Michigan: The "Tiered" Choice

Michigan used to require "Unlimited" PIP (the most expensive in the USA). Now you have choices: $50k, $250k, $500k, or Unlimited.

Warning: If you choose a lower limit (like $50k) to save money, and you have a catastrophic brain injury, you are on your own after $50k is gone. We strongly recommend Unlimited or at least $500k limits.

Verify your options at Michigan.gov/AutoInsurance.

Part 4: The "Coordination" Trap

In states like MI and NJ, you can choose to make your Health Insurance "Primary" for auto accidents. This lowers your car insurance premium significantly.

Should you do it?

YES, Coordinate If:

- ✓ You have a "Platinum" health plan (low deductible).

- ✓ Your health plan specifically confirms they cover auto accidents (ERISA plans often exclude this).

- ✓ You want to save $200-$500/year.

NO, Keep PIP Primary If:

- ✗ You have a High Deductible Health Plan (HDHP).

- ✗ You have Medicare or Medicaid (rules are complex and often result in liens).

- ✗ You want simplified billing (one adjuster handles everything).

Part 5: When "PIP" Is "Med Pay"

If you live in a "Tort" state (like California, Texas, Illinois), you don't have PIP. You have Medical Payments (Med Pay).

The Difference: Med Pay is strictly for medical bills. It does not cover lost wages or household services in most states. It is weaker than PIP, but still vital for covering your health insurance deductible.

Conclusion

Don't treat PIP as an annoyance. Treat it as the only safety net that pays you immediately.

While Liability insurance protects your net worth from lawsuits, PIP protects your cash flow from interruption. If you live paycheck to paycheck, or if you have a high-deductible health plan, maxing out your PIP is the smartest financial defense you can buy.

Audit Your PIP Coverage Now

Check your current Declarations Page. Do you have a $2,000 deductible? Is your limit too low?

Sources: Florida Highway Safety and Motor Vehicles (FLHSMV.gov), State of Michigan (Michigan.gov). Disclaimer: Educational content only.