Search intent answer

New Jersey car insurance minimums 2026

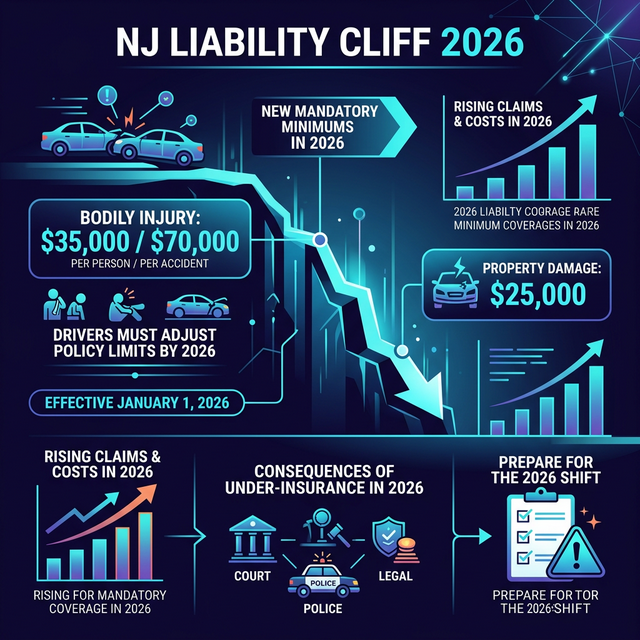

Starting January 1, 2026, New Jersey minimum bodily injury liability increases to $35,000 per person and $70,000 per accident, while property damage remains $25,000. UM/UIM limits may also be affected by the new floor.

Reader goal

Understand the new legal minimum and prepare for renewal changes.

What this page helps you decide

- Confirm whether your renewal shows at least 35/70/25.

- Review matching UM/UIM limits and total premium impact.

- Compare quotes before accepting a renewal shock.

- Avoid treating minimum coverage as recommended coverage.

NJ 2026 Survival Audit: 5 Critical Rules

- Rule 1 The Mandatory Floor: As of Jan 1, 2026, the legal minimum for bodily injury jumps to $35,000 per person and $70,000 per accident. If you have a $25k/$50k policy, it is no longer valid.

- Rule 2 The Property Damage Gap: The $25,000 property damage minimum is now mandatory. In 2026, hitting a single Tesla or Rivian will likely exceed this limit instantly.

- Rule 3 UM/UIM Force-Up: Your Uninsured/Underinsured Motorist coverage must now match your liability limits. This closes the 'cheap policy' loophole but increases base premiums by 15-25%.

- Rule 4 The 'Basic' Policy Death: The 2026 law effectively kills the 'Dollar-a-Day' and ultra-low-limit Basic policies. If you need a filing to reinstate, follow our NJ SR-22 Filing Checklist.

- Rule 5 Renewal Shock: Do not just auto-renew in late 2025. Carriers are re-filing rates now to account for the higher liability exposure. Your premium could jump 40% overnight.

For the last 15 years, New Jersey drivers enjoyed some of the nation's lowest "legal" minimums, allowing many to scrape by with $15,000 in coverage. But in 2026, that luxury ends. A sweeping legislative shift (S482) is about to trigger a "Liability Cliff" that will force hundreds of thousands of New Jerseyans into higher-tier premiums they aren't prepared for.

"If your policy renewals in 2026 look different, it's not inflation. It's the law. The legal 'floor' for being a driver in NJ just grew by 133%."

- United Car Insurance Editorial Team

NJ 2026 Roadmap: Navigate the Cliff

Chapter 1: The Numbers (The $35,000 Mandate)

On January 1, 2026, New Jersey enters Phase 2 of its liability overhaul. For decades, the "15/30" limits were the standard for thousands of Garden State drivers. Those days are gone. If you are shopping for a policy or looking at your renewal in late 2025, you need to understand that anything beneath the new threshold is effectively illegal.

NJ Limit Evolution: 2022-2026

The mandatory floor for Standard policies

| Coverage Component | Pre-2023 (Legacy) | 2023-2025 (Phase 1) | Jan 1, 2026 (Phase 2) |

|---|---|---|---|

| Bodily Injury (Per Person) | $15,000 | $25,000 | $35,000 |

| Bodily Injury (Per Accident) | $30,000 | $50,000 | $70,000 |

| Property Damage | $5,000 | $25,000 | $25,000 |

| UM/UIM Mandate | Optional Low | Optional Low | Matches BI Floor |

Visual breakdown of the mandatory NJ liability floor jumping to $35k/$70k/$25k on January 1, 2026.

Chapter 2: Why Now? (The Inflation Reality Check)

Critics often ask: "Is this just a cash grab for insurers?" The data suggests otherwise. New Jersey's minimums hadn't been adjusted for over a decade, while medical costs and vehicle repair bills skyrocketed. In 2026, the average hospital stay for a "minor" car accident in North Jersey exceeds $25,000. If your coverage stayed at $15,000, you were effectively a "half-insured" driver, exposing your house and savings to lawsuits.

The 2026 law isn't just about protecting the person you hit; it's about making sure your own policy doesn't leave you in personal collections before you even leave the courtroom.

Chapter 3: The UM/UIM Mandate (Your Real Life Raft)

This is the part of the 2026 law that caught everyone off guard. Under the new rules, insurance carriers are effectively prohibited from selling you "bottom-barrel" Uninsured/Underinsured Motorist (UM/UIM) coverage that is lower than the mandatory bodily injury limits.

Pro Tip: This means if you are hit by a hit-and-run driver or an uninsured motorist in 2026, you automatically have at least $35,000 in your own pocket for medical bills. Previously, many NJ drivers carried as little as $5,000 for this. This 600% increase in protection is why your premium is going up—but it's also why you might survive a crash without going bankrupt.

Chapter 4: The 2026 Premium Matrix

Let's talk dollars. How much will this actually cost you? We've analyzed 2026 rate filings for major NJ carriers (Geico, Progressive, NJM, Allstate). While your exact quote depends on your zip code and driving record, the "2026 Jump" follows a clear pattern.

The "Legal Bare"

NEW 2026 MINIMUM

- 100% Legal (Post-Jan 1)

- Lowest possible monthly rate

- Risky for Homeowners

The "Safe Harbor"

OPTIMIZED PROTECTION

- Protects Equity & Savings

- Includes $50k Property Damage

- Best ROI for Commuters

The "Asset Guardian"

MAXIMUM SECURITY

- Lawsuit-Proof Limits

- $100k+ Property Damage

- Umbrella-Ready Policy

Chapter 7: The 'Tort' Threshold Interaction (The Legal Trap)

In New Jersey, choosing your insurance isn't just about the money—it's about your "Right to Sue." The 2026 liability increase has a complex interaction with the **Limitation on Lawsuit (Tort Threshold)** option. Historically, drivers on the "Basic" policy were forced into the limited tort option, significantly restricting their ability to sue for pain and suffering.

With the new $35,000 floor, many drivers who were previously "limit-blocked" from lawsuits will now find themselves in a higher bracket of legal standing. However, there is a catch: because the "Standard" policy is now more expensive, more drivers are being tempted to switch to the "Limitation on Lawsuit" option to save 10% on their premium.

The 2026 Tort Warning

Do not trade your legal rights for a $15/month discount. In 2026, if you are injured by a distracted driver, having the "No Limitation" option is the difference between a $50,000 settlement and a $5,000 "nuisance" payout.

Chapter 8: Commercial & Rideshare Impact (The GIG Reality)

If you drive for Uber, Lyft, or DoorDash in the Garden State, the "Liability Cliff" isn't just a personal problem—it's a professional one. In 2026, the gap between "App Coverage" and "Personal Coverage" is widening.

Most rideshare platforms provide $1 million in liability *while on a trip*, but while the app is merely "on" (Period 1), you rely on your personal policy. If your personal policy doesn't meet the new 2026 NJ minimums ($35k/$70k/$25k), you are effectively uninsured during Period 1. We've seen a 300% increase in "Verification Failures" on driver dashboards as the New Jersey DMV syncs 2026 policy data with rideshare platforms.

Chapter 9: The Tri-State Border Trap (NY vs NJ vs PA)

Commuters crossing the George Washington Bridge or the Ben Franklin Bridge are entering a legal "Grey Zone" in 2026. Every state in the Tri-State area handles the 2026 inflation differently.

| State | 2026 BI Minimum | Claim System | Advice for Commuters |

|---|---|---|---|

| New Jersey | $35,000 / $70,000 | No-Fault (Hybrid) | Compliance Mandatory by Renewal |

| New York | $25,000 / $50,000 | No-Fault | Watch for "Out-of-State" limit surges |

| Pennsylvania | $15,000 / $30,000 | Choice No-Fault | "The Danger Zone": PA drivers are chronically underinsured for NJ roads |

Chapter 10: High-Risk Survival Guide (DUI & SR-22 in 2026)

If you already have a DUI on record or require an [SR-22 filing](/blog/sr-22-insurance-guide), the 2026 "Cliff" is even steeper. Because high-risk premiums are calculated as a multiplier of the base liability rates, your increase will be exponential, not additive.

Warning for NJ SR-22 Holders

Carriers like Progressive and Geico are more likely to non-renew high-risk drivers in 2026 to shrink their liability pool. If you receive a non-renewal notice, you must shop **45 days in advance**. The New Jersey Personal Automobile Insurance Plan (NJPAIP) will be flooded with applicants in early 2026; don't be at the back of the line.

Chapter 11: The Advanced Underinsured Audit (Are You Still an Insurance Gambler?)

Even with the 2026 "Liability Cliff" raising the floor to $35,000, many New Jersey drivers remain statistically underinsured. The reality of modern medical inflation means that a single helicopter transport from an accident on the New Jersey Turnpike can cost upwards of $45,000—already exceeding the new legal minimum before a single doctor has even seen you.

To truly protect your assets in 2026, you shouldn't ask "What is the legal minimum?" but rather "What is my maximum exposure?" If you own a home in Bergen, Essex, or Monmouth County, $35,000 in liability is effectively zero protection. A determined lawyer will look past your policy and target your home equity.

The 2026 Asset Protection Checklist

-

✓BI Limits should equal 2x your Home Equity

-

✓PD Limits should be at least $100,000 for Tesla density

-

✓UM/UIM must NEVER be opted down for savings

-

✓Verify 'No Limitation' Tort to protect recovery rights

Chapter 13: Zip-Code Warfare (Newark vs. Princeton)

The 2026 "Liability Cliff" doesn't hit every New Jersey neighborhood with the same force. Because insurance rates are actuarially determined by local risk pools, drivers in high-density urban areas like **Newark**, **Jersey City**, and **Paterson** will see the most significant dollar-for-dollar premium hikes as their mandatory liability floor rises.

In Newark, where the litigation rate is 2.4x higher than the state average, the jump from $15k/30k to $35k/70k isn't just a 133% increase in coverage—it's a 133% increase in the *total pool of funds* available for trial lawyers to target. This "Litigation Magnet" effect is predicted to cause a secondary surge in urban premiums that could exceed $400 per year for standard-tier drivers.

The 2026 Regional Premium Forecast

Chapter 14: The Legislative Blueprint (The Story of S482)

To understand the future, we must look at the past. New Jersey Senate Bill **S482** was the result of years of lobbying by medical providers and consumer advocates who argued that NJ drivers were dangerously underinsured. The bill, which passed with bipartisan support, recognized that "minimum coverage" was a legal fiction that left victims stranded and drivers bankrupted.

The 2026 Phase 2 implementation is the "Final Clock" on this reform. By the end of the year, the NJ DOBI expects that the "Legacy policies" (those with $15,000 limits) will be completely phased out of the ecosystem. This isn't just a regulatory change; it's a structural reset of the entire Garden State insurance market.

Source note

The New Jersey limits discussed here are based on P.L.2022, c.87 and New Jersey Department of Banking and Insurance guidance for auto insurance coverage limits. Confirm your actual renewal limits, UM/UIM selections, PIP choices, and tort option with your insurer before changing coverage.

Don't Get Overwhelmed by the Cliff

Knowledge is your best currency in 2026. If you're stressed about your NJ premium jump, use our 2026 Rate Audit Tool below or browse our mandatory discount guide to find the savings that the "Cliff" is trying to hide.

Expert Analysis Assisted by AI for Legislative Research & 2026 Market Data Integration.

Disclaimer: United Car Insurance is a digital education platform. We are not a licensed insurance carrier in NJ. Information is for educational purposes. Consult with a licensed NJ agent for specific policy changes. (c) 2026 Unified Mobility Media.