Search intent answer

diminished value claim

A diminished value claim asks for the market value your car lost because it now has an accident history. Most drivers pursue it against the at-fault driver’s insurer and support the demand with repair records, photos, comparable listings, and an appraisal.

Reader goal

Understand whether a diminished value claim is worth filing and what proof strengthens it.

What this page helps you decide

- Confirm whether the claim is first-party or third-party.

- Estimate value loss without relying only on the insurer’s 17c formula.

- Gather repair invoices, photos, vehicle history, and comparable listings.

- Prepare a demand letter and negotiation file.

Key Takeaways

- ✓ It's Real Money: A car with an "Accident" on its Carfax report sells for 15-30% less than a clean car. You can claim this loss.

- ✓ The 17c Trap: Most insurers use the "17c Formula" (10% Cap) to calculate your offer. This formula is deeply flawed and often legally beatable.

- ✓ Know Your Rights: Georgia is the only "First-Party" mandate state. In almost all other states, you must file a "Third-Party" claim against the at-fault driver.

Imagine this scenario: You drive a 2024 Toyota Camry worth $28,000. You get rear-ended at a stoplight. The other driver's insurance pays $6,000 to fix the bumper, trunk, and sensors. The body shop does amazing work—the car looks brand new.

Six months later, you go to trade it in. The dealer pulls the Carfax report, sees "Accident Reported: Moderate Damage," and drops their trade-in offer to $22,000. You just lost $6,000, even though the car was "fixed."

This invisible loss is called **Diminished Value (DV)**. Insurance companies save billions every year because 90% of drivers don't know this coverage exists. In 2026, with vehicle history reports becoming more transparent and widely used by consumers, the financial hit from an accident history is steeper than ever. This guide will teach you how to calculate what you are owed and, more importantly, how to collect it.

Diminished Value Logic Hierarchy (2026)

Guide Contents

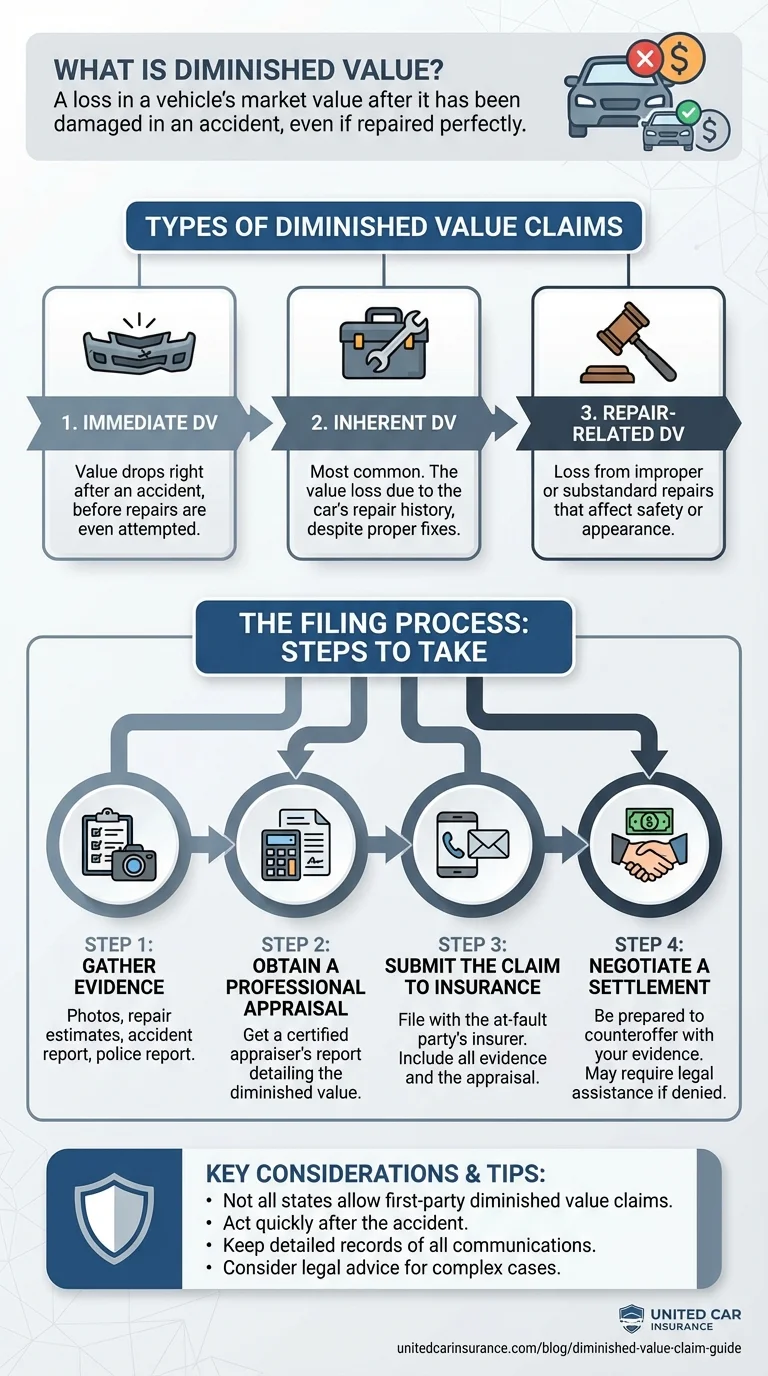

1. The Three Types of Diminished Value

Before you file, you must identify why your car lost value. There are three legal definitions, but only one is commonly paid out.

1. Inherent Diminished Value (The "Big One")

Definition: The loss of value simply because the car has a repair history. The car is fixed perfectly, but the "stigma" remains.

Verdict: This is the standard claim most drivers pursue.

2. Repair-Related Diminished Value

Definition: The loss of value because the repairs were done poorly (mismatched paint, rattling, panel gaps).

Verdict: Insurance usually won't pay this directly; they will force the body shop to redo the work under their guarantee.

3. Immediate Diminished Value

Definition: The difference in resale value immediately after the accident, before repairs happen.

Verdict: Rarely used practically unless you sell the wrecked car as-is.

2. Legal Landscape: First vs. Third Party

This is the most critical distinction in your claim. Who are you suing?

Third-Party Claims

"The Other Guy's Fault"

Another driver hit you. You are claiming against their insurance policy.

Since you have no contract with their insurer, they owe you "to be made whole" under tort law.

First-Party Claims

"My Own Insurance"

You hit a tree, or an uninsured driver hit you. You claim against your policy.

Most policies explicitly exclude DV in the fine print. Georgia is the major exception.

3. Deep Dive: The 17c Formula

If you file a claim, the adjuster will likely plug your numbers into the "17c Formula." This formula originated from the Georgia case State Farm v. Mabry (2001). While originally intended as a "minimum process," insurers nationwide now abuse it as a "maximum limit."

The 17c Equation

Take NADA Retail Value.

Divide by 10.

Severe Structure: 1.0

Moderate: 0.5

Minor: 0.25

0-20k: 1.0

40-60k: 0.6

100k+: 0.0

Critique: This formula assumes the maximum possible loss represents only 10% of the car's value. In reality, luxury buyers often demand 20-30% discounts for wrecked cars.

4. Calculator: Estimate Your Claim

Let's run a real scenario to see how this works.

| Vehicle | Scenario | Pre-Accident Value | 17c Offer | Real Market Loss |

|---|---|---|---|---|

| 2025 Tesla Model Y | 15k miles, Moderate Damage | $45,000 | $2,250 | $6,000+ |

| 2022 Ford F-150 | 50k miles, Severe Frame | $38,000 | $2,280 | $7,500+ |

| 2016 Honda Civic | 110k miles, Minor Dent | $10,000 | $0.00 | $500 |

5. State-Specific Laws (2026 Update)

Geography is destiny when it comes to DV claims.

Georgia (The Gold Standard) ▼

Georgia is unique. O.C.G.A. 33-34-43 requires insurers to automatically assess diminished value on First-Party claims. You don't have to ask. However, they almost always use 17c. You can demand more, but the onus is on you to prove it.

North Carolina ▼

Allow First-Party claims but is less regulated than Georgia. The NC Bureau of Insurance provides guidance, but insurers often resist. Third-party claims are standard.

Washington, Kansas, Oregon ▼

These states have favorable case law allowing First-Party claims unless the policy specifically excludes it (which most now do). Read your policy definitions carefully.

Michigan (The Exception) ▼

Due to No-Fault laws, you largely cannot claim DV. Your only recourse is the "Mini-Tort" provision which caps recovery at $3,000 (as of 2026 adjustments) and is difficult to apply to non-physical damage.

6. Step-by-Step Filing Guide

Ready to fight? Do not send a generic email. Follow this escalation ladder.

Wait for Excellence

Wait until repairs are 100% done. If the potential buyer sees a mismatched bumper, you have a repair issue, not a DV issue. The car must be "perfect" for DV to apply.

Get a USPAP Appraisal

Do not use a free online calculator. Insurers ignore them. Pay $300-$500 for a licensed auto appraiser to write a certified report. This report is your legal weapon.

Send the Demand Letter

Send a physical certified letter to the supervisor. Attach the appraisal. State: "I am demanding $X based on the attached certified evidence."

Small Claims Court (The Nuclear Option)

If they offer $500 on a $5,000 claim, file in Small Claims court against the driver (not the insurer). The insurer is legally obligated to defend their driver, and they will typically settle to avoid the legal cost.

Official Sources

Don't Just Survive the Claim.

Win It.

The 2026 insurance game is won by the driver with the best evidence. Equipping your vehicle with a 4K Dash Cam and a certified Roadside Kit isn't just safety—it's financial defense.

Disclaimer: Diminished value laws are complex and vary by jurisdiction. This article explains general insurance principles and should not be considered legal advice.