Search intent answer

total loss car insurance payout

A car is usually totaled when repair cost plus salvage value approaches or exceeds its actual cash value. The settlement should reflect the vehicle’s pre-loss market value, adjusted for mileage, options, condition, and comparable sales.

Reader goal

Audit the insurer’s valuation report and decide whether to accept, dispute, or escalate.

What this page helps you decide

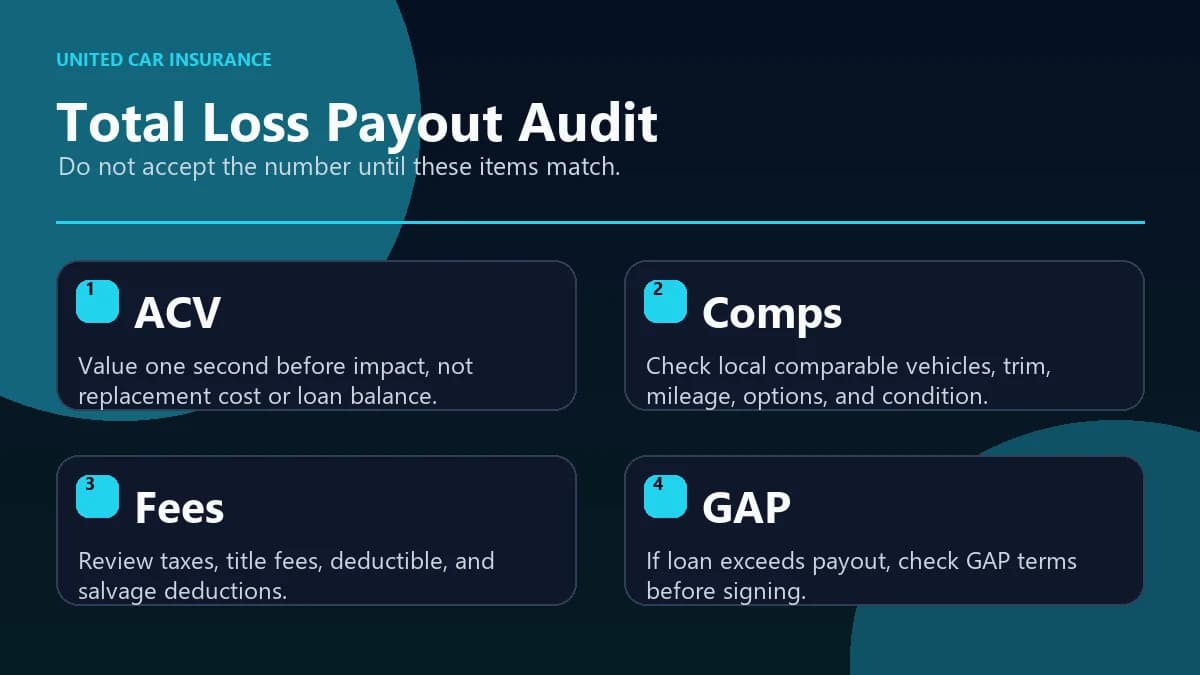

- Separate actual cash value from replacement cost and loan balance.

- Check comparable vehicles, options, mileage, taxes, and fees.

- Understand state threshold or total-loss formula rules.

- Review whether GAP applies if the loan exceeds the payout.

Key Takeaways

- ✓ The "Sensor Cliff": In 2026, repair costs for ADAS (sensors/cameras) mean cars are being totaled at just 50-60% of their value, even in states with higher thresholds.

- ✓ ACV != Replacement Cost: You are owed the "market value" of your specific car, not the price of a brand new one.

- ✓ Valuation Reports are Flawed: Up to 30% of automated valuation reports (CCC One/Mitchell) miss key options or use bad comparables. You must audit them.

It’s a phone call no driver wants to receive. You sent your car to the shop for what looked like a fender bender—maybe a cracked bumper and a smashed headlight. But today, the adjuster called with surprising news: "Your vehicle is a total loss."

Confusion sets in. "How? The engine runs fine. The airbags didn't even deploy!"

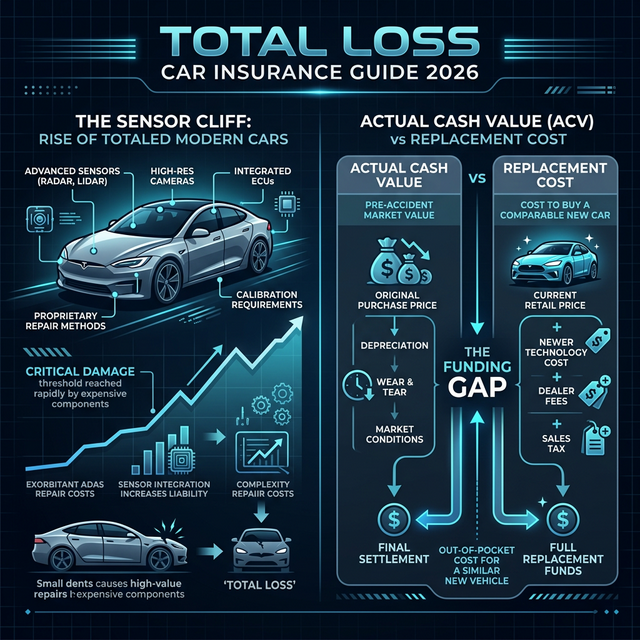

Welcome to the 2026 auto insurance landscape. Thanks to the stratospheric rise in repair costs driven by Advanced Driver Assistance Systems (ADAS) and complex EV battery architectures, the "Total Loss Threshold" has plummeted. Cars that would have been repaired five years ago are now being sent straight to the salvage yard.

If you are navigating a total loss claim right now, you are at a rigorous disadvantage. Insurance carriers use sophisticated algorithms to calculate your payout, often resulting in an offer that barely covers your loan, let alone a replacement vehicle. This guide is your equalizer. We will deconstruct the entire process, from the "75% Rule" to the "CCC One" market valuation report, giving you the actionable data you need to negotiate a fair settlement.

In This Guide

1. What Actually Constitutes a "Total Loss"?

A "Total Loss" (or "write-off") doesn't necessarily mean the car is un-drivable or flattened like a pancake. It is purely a math equation used by insurance adjusters to minimize financial risk.

The Core Definition

A vehicle is a total loss when the Cost of Repairs + Salvage Value exceeds the Actual Cash Value (ACV) of the vehicle.

Insurers look at your car as an asset. Every car involving a collision has a "Salvage Value"—the price a junkyard or auction house (like Copart or IAA) will pay for the scrap metal and parts. If fixing your car costs more than what the car is worth minus what they can get for the scrap, they will total it.

Constructive Total Loss

This is the term adjusters use when the car could physically be fixed, but it doesn't make economic sense to do so. In 2026, this is the most common scenario. The frame might be straight, the engine might start, but if the wiring harness for the autonomous driving sensors is severed, the 200 hours of labor required to replace it might push the repair bill over the threshold.

2. The Math: Actual Cash Value (ACV) vs. Replacement Cost

This is the single biggest point of friction between insurers and drivers. You want enough money to buy a new car. The insurer is only checking their legal obligation to pay you for the old car.

Actual Cash Value (ACV)

The value of your car one second before the impact.

- ❌ Deducts for depreciation (Mileage/Age)

- ❌ Deducts for pre-existing wear (dents, stains)

- ❌ Does NOT care about your loan balance

$18,400

Replacement Cost

The cost to buy a brand new version of your car today.

- ✓ No deduction for depreciation

- ✓ Pays full sticker price of new model

- ✓ Requires specific endorsement

$27,500

In 2026, the rise of ADAS (Advanced Driver Assistance Systems) means smaller impacts now trigger the 75% threshold, resulting in more "Constructive Total Loss" designations.

Unless you have explicitly purchased Gap Insurance or New Car Replacement coverage, you are getting the ACV. This creates a "Depreciation Cliff." If your car is 2 years old, it has likely lost 30% of its value, yet your loan might barely be paid down.

3. State Laws: The 75% Rule vs. TLF

Legally, roughly half of U.S. states use a "hard" percentage threshold to define a total loss. The other half use a formula that gives insurers more flexibility.

| System | The Rule | States (Examples) |

|---|---|---|

| The 100% Rule | Repair costs must equal 100% of value. | Texas, Colorado |

| The 80% Rule | Repairs must exceed 80% of value. | Florida, Oregon |

| The 75% Rule | Repairs must exceed 75% of value. | NY, NC, VA, SC, AL |

| The 70% Rule | Repairs must exceed 70% of value. | MI, IN, AR, WI |

| The TLF (Formula) | Repair + Salvage > ACV | CA, GA, OH, IL, PA |

Warning: Just because your state has a 75% threshold doesn't mean the insurer must repair it if damages are 74%. Insurers can generally total a car earlier than the state threshold if they deem it unsafe or economically risky. The state threshold is just the point where they are mandated to brand the title as Salvage.

4. Why New Cars Are "Totaling" Faster (The ADAS Effect)

In 2020, a cracked bumper was a $800 repair. In 2026, that same bumper contains:

- Ultrasonic parking sensors

- Blind-spot monitoring radar

- Lane-keep assist cameras

According to reports from Mitchell International and CCC Intelligent Solutions, the average cost of collision repair has risen over 5% annually for the last four years. The culprit is not just parts, but Calibration.

The "Scanning" Tax

Every modern car requires a pre-repair and post-repair diagnostic scan. Shops charge 1.0 to 1.5 labor hours for this. This adds $150-$300 to every single estimate, regardless of damage severity.

Mandatory Calibrations

If a windshield is replaced or a bumper removed, the cameras must be recalibrated. This requires specialized targets and floor space. Average cost: $500 - $800 per incident.

This is why insurers are "totaling" cars at 50% or 60% of value. They know that once the teardown begins, hidden electronic damage will likely blow the budget. It is cheaper for them to pay you the ACV now than to start a repair that balloons to $15,000 later.

5. The Valuation Report (CCC/Mitchell)

How does the insurer decide your car is worth $14,231 and not $16,000? They use third-party vendors, primarily CCC Intelligent Solutions, Mitchell, or Audatex.

These systems generate a 15-20 page PDF called the Market Valuation Report. It is imperative that you ask for this document immediately. Do not accept a verbal number over the phone.

Common Flaws in CCC Reports

Multiple class-action lawsuits have alleged that these systems systematically undervalue vehicles by:

- Condition Adjustment: Arbitrarily rating your seats/dash/tires as "Fair" instead of "Dealer Ready" to subtract $500-$1,000.

- Geographic Expansion: Using a comparable car sold 300 miles away in a cheaper rural market, rather than your expensive metro area.

- Ghost Cars: Using "Listings" that have already been sold or never existed, rather than confirmed sales.

6. Battle Plan: Negotiating Your Payout

You do not have to accept the first offer. In fact, you shouldn't. Follow this checklist to build your counter-offer.

Your Negotiation Checklist

Tell the adjuster: "Please email me the full CCC/Mitchell valuation report used to determine this offer."

Go through the report line-by-line. Did they miss your Navigation Package? Leather seats? Tow hitch? Roof rack? Each missing option is worth $50-$500.

Did you put new tires on 3 months ago? Replace the transmission last year? Submit these receipts. You won't get dollar-for-dollar value, but you might get 20-30% of the cost added back.

Go to Autotrader and CarGurus. Find 3 vehicles within 50 miles with similar year/trim/mileage. Save the PDFs. If they are priced $2k higher than your offer, send them to the adjuster.

If they won't budge, check your policy for the "Appraisal Clause." It allows you to hire an independent appraiser to negotiate a binding value with their appraiser. This is the nuclear option.

7. The Financial Gap & Leasing

If you owe $25,000 on your loan, but the ACV settlement is $20,000, the lender will take the full $20,000 check. You are then left with no car and a $5,000 debt.

This is where Gap Insurance is critical. If you purchased it (either through the dealer or your insurer), it covers that $5,000 difference.

Leased Vehicles

Most lease contracts include Gap coverage (sometimes called "Gap Waiver") automatically. Check your lease agreement. If your leased car is totaled, you generally walk away owing nothing, but you also get nothing back—no down payment recovery, no equity.

8. Keeping the Car (Owner Retained Salvage)

If you love the car and the damage is cosmetic (e.g., hail damage or a dented rear quarter panel), you can ask to keep it. This is called "Owner Retained Salvage."

The Buy-Back Math Example

You get $11k and keep the car. You then use that money to fix it (or not). Note: You will have a "Salvage Title" which reduces resale value significantly.

Sources & Further Reading

Disclaimer: This article provides general information and does not constitute legal or financial advice. Insurance laws vary by state. Consult with a licensed public adjuster or attorney for specific case advice.